1% Risk. No Extra Work. 3× Returns.

One small bet can change your life

The biggest myth in investing is that higher returns require taking more risk.

They don’t.

They require better asymmetry.

You want to minimize risk while maximizing rewards.

Most people should not be picking stocks because it is hard and time consuming. Most people should just invest in an index fund.

There is nothing wrong with that.

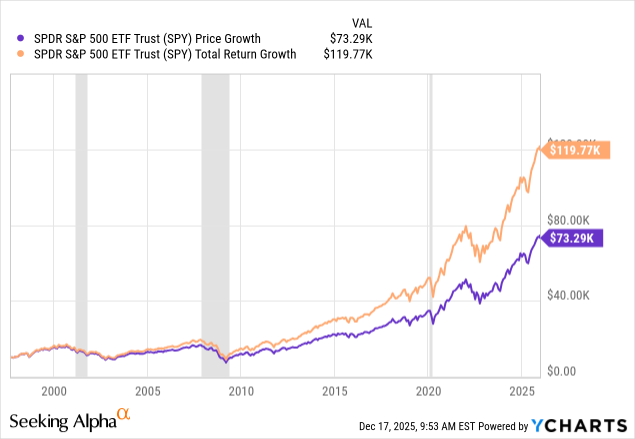

If you had invested $10,000 in the S&P 500 in September 1997, you would have about 73k today (or about $120k with dividends reinvested.)

Why did I choose to start this experiment from September 1997. Because that’s when Steve Jobs returned as CEO of Apple.

If let’s say then, you had decided to invest $100 in Apple with the remaining $9,900 in the S&P 500.

Your $100 in Apple would have turned into $139k while your $9,900 in the S&P 500 turning into about $73k, for a total of $212k. With this extra 1% risk you took, you nearly tripled your investments!

Unfortunately, you cannot go into the past to make this investment. But the same principles are applicable today.

The investments you make today are going to change your life a few decades from now.

Investing in Apple in September 1997 would have been very risky.

Sales were down 28% from 1996, with the company losing money and on the brink of bankruptcy. The worst that could have happened was that your $100 investment goes to zero. If wouldn’t be so bad. Your returns would still be about the same as investing only in the S&P 500. It was a minute risk.

The only thing that changed with Apple in 1997 was that Steve Jobs was back. He had proven himself in the past as a visionary leader at Apple and later as a competent CEO at Pixar and NeXT. What was there to lose? With hindsight, it seems like this small investment would have been worth it.

By the end of 1997, your $100 was down over 40% and at the peak of the dotcom bubble reached a value of $653 before crashing back to around $130. And by mid 2003 (nearly six years from your initial investment), your $100 had turned into a mere $121.

But the fundamentals of Apple were improving. The iPod was launched in 2001. And everything changed with the launch of the iPhone in 2007.

Steve Jobs passed away, there was a trade war, a pandemic. But you kept holding your shares. With no extra work.

With this one little bet you made in 1997, you tripled your investment.

The best part is that it all happened with just one investment—one company.

You may argue that the only reason it works was luck. You happened to have invested in Apple. But as we saw, it could have gone to zero in 1997 and was almost flat for six years with a massive drop of 81% in between. Luck was certainly part of the equation. Nobody could have predicted the iPhone (although, you could argue that Steve Jobs could!) But it also worked for the following reasons:

Visionary leadership under Steve Jobs

World-changing products

Efficient capital allocation under Tim Cook

All of which kept improving the fundamentals.

Apple has bigger revenue growth than the market with higher margins and better returns on capital.

These fundamentals put together compounded—At a higher rate than the market. So did the stock price.

If you want zero risk, you can always buy US government bonds. Any other investment will have some risk. Investing in the S&P 500 is the least risky way of investing in equity. This is what most people should do. That doesn’t mean you can’t take a little extra risk. What’s the worst that can happen? Your 1% goes to zero? But the best that can happen with the right investment can be life changing.

There is an inherent risk-reward asymmetry in stock investing with limited downside and unlimited upside.

To maximize this asymmetry, you need to be patient. You need to sit for years without doing anything. It is harder than it sounds!

I don’t know if you noticed it but we have a problem, however, with our example. If you invested 1% of your portfolio in Apple in 1997, today that would be 66%. With 6% of the S&P 500 in Apple, your total exposure would be about 68%.

Is that too concentrated? Is that too risky?

We will answer these questions in another post. And we’ll talk about a simple way to “diversify” your portfolio.

I completely agree.

This is the theory my portfolio is also based on.